How insurers can use telematics technology to improve customer experience and increase market competitiveness

As technology is evolving in the car insurance and data-defined vehicles markets, the generational cross-section of people who use them is also undergoing transformation. Currently, two generations, in particular, are coming to the fore: Millennials and Gen Z. They are interested in service and product offerings that are as personalized and tailor-made as possible, rather than generic. Adding to that the rapid development of vehicle connectivity, now is the perfect time for insurers to roll out and scale up their telematics products offer.

Based on research by Allison+Partners, consumers within the youngest generation view the car simply as yet another life-enhancing device. What's more, about 70% of Generation Z consumers don't have a driver's license, and 30% of this group have no intention or desire to get one. This makes them more interested in carpooling using an autonomous vehicle. More than 45 percent of respondents feel comfortable with this. Thus, "urban mobility" players such as Uber and Lyft, as also e-scooter providers and on-demand car rental services are in demand . All of these are capable of filling the empty gap in the public transport infrastructure.

There is another interesting point. Those who do decide to get a driver's license and buy a car on their own, however, face the hassle of costly insurance . The amounts are especially exorbitant for the least experienced drivers, who in fact pay more for their year of birth stamped on their ID cards. There is even talk of the "age tax" phenomenon. Interestingly, young age does not always go hand in hand with traffic violations or dangerous driving behavior. Generations Y and Z are therefore advocating that car insurance should be reassessed, with more emphasis on personalization .

Telematics - technology that supports contemporary society's needs

Consumers today, particularly younger ones, expect cars to be as innovative as possible, as this directly translates into comfort and safety. Above all, personalized experiences, reliable connection, and comfort count. All this is a recipe for success in the future of mobility as a service .

Individual online services should be consolidated into comprehensive mobility platforms. This will ensure that the user no longer has to switch between applications, and autonomous driving will generate new opportunities for innovative business models.

Utilizing telematics data opens the door to improving customer experience, unlocking new revenue streams, and increasing market competitiveness.

A modular and extensible telematics architecture provides tremendous opportunities for all pro-change agents.

This allows you to organize data handling, filter it and add missing information at various stages of processing. And it will not be an overstatement to say that in a technology-oriented information society, it is data that is the most valuable resource these days.

They can be used in all business processes, interacting with the customer experience and responding to their needs. Especially those who represent the younger generations of the future, namely Millennials and Gen Z.

Telematics platforms and the future of the automotive industry

The processed information is also used to train AI/ML models and to monitor system behavior. When you add to this the fact that they are extracted and included in real-time, you gain the added value of the rapid response. This then results in service satisfaction and sustained business performance.

On the other hand, driving data collected from various sources offer a full insight into what is actually happening on the road, how drivers behave, and what decisions they make while driving. Insurers benefit from this, but so do car manufacturers and companies that deal with shared mobility in its broader sense.

All these advantages are seemingly speaking for themselves. And this is just the beginning because the future of telematics is looking very bright. The results of IoT Analytics research indicate that by 2025 the total number of IoT devices will have exceeded 27 billion globally. For comparison, it is important to add that currently there are 1.06 billion passenger cars on the roads around the world. Specialists predict that in just these few years this value will increase by more than 400 million connected vehicles .

What will the end customer and the insurers themselves gain from applying telematics technology in automotive insurance?

Crash detection

The real-time feature of a telematics platform allows to detect accidents instantly and take proactive actions to mitigate the damages. Car location and sensor data can be used to trigger the crash alerts, coordinate emergency services dispatch, and reconstruct the crash timeline.

Such solutions are already being implemented, for example at IBM. Their Telematics Hub enables the management of crash and accident data in real-time and with a low probability of error. The tool can distinguish a false event from a real one, generate incident reports, and evaluate driver behavior.

Roadside assistance

According to Highway England, there are over 224,000 car breakdowns a year on England's busiest roads. That's an average of 25 cars per hour. In contrast, in another Anglo-Saxon country, the U.S., there are 1.76 million calls for roadside assistance per year.

Roadside assistance is an optional add-on to drivers' personal car insurance. It’s a popular service among the drivers but it needs to be further developed which requires leveraging real-time data processing. Those insurance providers that offer remote service or that minimize time spent on the side of the road are gaining a competitive advantage.

Monitoring vehicle activity allows pinpointing its location in case of an emergency. Once notified of the breakdown, assistance can be dispatched to the customer position, and the nearest available replacement vehicle can be booked.

UBI & BBI

Behavior-based (pay-how-you-drive) and usage-based insurance - UBI - (pay-as-you-drive) are the future of car insurance programs . Together with value-added services like automated crash detection or roadside assistance, they will determine the competitiveness and market share of insurance companies.

Handling large volumes of real-time data from every telematics device, like connected cars, mobile apps, and black boxes to extract crucial information and offer insights to customers, requires a robust and scalable telematics platform.

Experts point out many advantages of UBI schemes over the conventional solutions offered so far. The most important of these are:

- Potential discounts.

- The authorities and insurance claims adjusters have facilitated accident investigations.

- Drivers become motivated to improve their performance and eliminate risky driving behaviors and unsafe habits.

- Enhancing customer loyalty.

- Providing personalized, value-added services to insurance plans to serve customer interests more effectively.

Stolen vehicle recovery

The demand for targeted technologies for vehicle tracking and recovery comes in handy for insurance companies, which face the problem of issuing sizable amounts of compensation for stolen vehicles on a daily basis.

It's not true that younger generations are fickle and unwilling to take out insurance. Generation Z consumers and Millenials accounted for 39% of consumers buying auto insurance in 2018. This figure is increasing year on year and applies not only to compulsory insurance but also to additional plans. The problem is that in many cases theft insurance offers, if there are any, are based on statistical indicators rather than actual data, for instance, the high crime rate of this type in a given area. Besides, customers are often dissatisfied with amounts based on market values that are lower than expected.

So here, too, data-driven individualization is needed, and that's what telematics provides.

For instance, by gathering data about customer behavior, insurers can build driver profiles that allow them to set up alerts that are triggered by unusual or suspicious behavior. Another thing is real-time vehicle tracking. The alarm service can be activated on-demand or automatically, and the car establishes a connection to the operations center. It is also possible to document theft. Information detected by the vehicle is collected and then exported and made available for viewing by the appropriate people.

Telematics technology is an answer to a need, but also a challenge

The Millennials and Generation Z expect a holistic customer experience. Digital offerings must bring together a variety of products designed to make life easier and accommodate each individual's consumer personality.

This is exactly the task facing telematics today, which is not just an incomprehensible and distant technology. It is essentially something that allows you to adapt to society's changing service and experience-related expectations.

However, the new expectations of shared mobility, autonomous vehicles, and personalized data insurance offers are linked to new sacrifices that end customers must also be prepared to make. These include, for example, the need to share more and more data. Yet, the younger generations are already declaring their readiness. According to the Majesco survey, almost half of generation Z are also willing to share data if they see value in doing so. Questions in the survey also referred to the car and driver data-based insurance industry.

There are also massive challenges for insurers themselves, where data processing is still only at an initial stage. The technological capabilities of individual insurance companies need to be continuously developed. Ideally, driving data, and the software used to collect and process it, should not be scattered but planned holistically. This ultimately leads to the conscious use of telematics and to better management of situations requiring insurance payouts.

Grape Up helps you realize the potential of telematics by applying the automotive and insurance industry expertise to create scalable, cloud-native solutions.

We design a fast lane for Financial Services

Build future-ready solutions that learn, predict, and respond in real-time.

Check related articles

Read our blog and stay informed about the industry's latest trends and solutions.

How to enable data-driven innovation for the mobility insurance

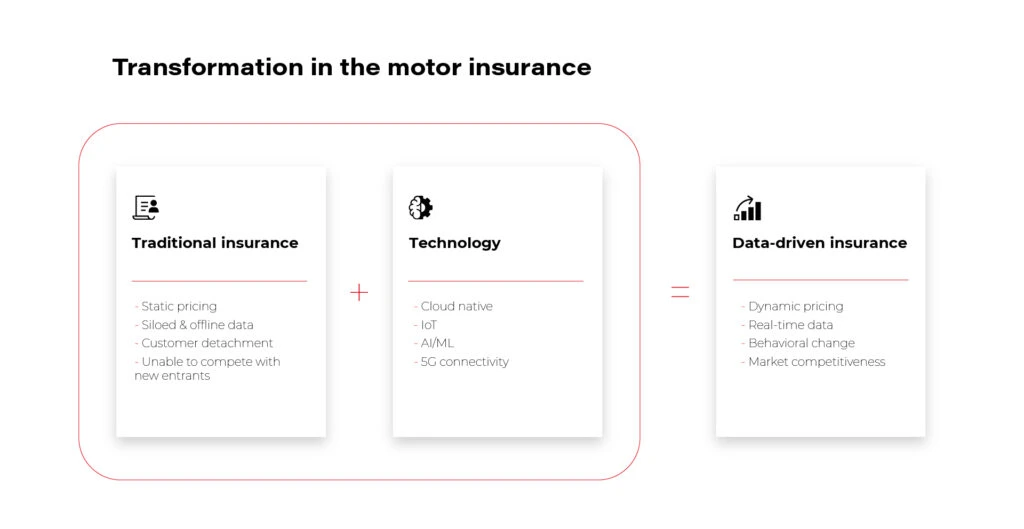

Digitalization has changed the way we shop, work, learn and take care of our health or travel. Cars are no longer used just to get from A to B. They are jam-packed with technology that connects us to the world, enhances safety, prevents breakdowns, and even provides entertainment. With the rise of the Internet of Things and artificial intelligence, a vehicle is no longer understood solely in terms of its performance and sleek design. It has become software on wheels, a gateway to new worlds - not just physical, but also virtual. And if the nature of insurance itself is changing, then the company offering insurance must keep up with these changes as well. Insurance needs digital innovation, as much as any other market area.

These days customers are looking for customization, personalization, and understanding their needs on an almost organic level. Data and advanced analytics allow us to effectively satisfy these needs. Thanks to them, it is possible to fine-tune the offer, not so much for a specific group, but for a particular person - their habits, daily schedule, interests, health restrictions, or aesthetic preferences. And in the case described by us - a person's driving style and commuting patterns .

If you think about it, the insurer has the perfect tool in their hands. If they can tap into the potential of the software-defined vehicle and equip it with the right applications, there will be nearly zero chance of inaccurate insurance risk estimates. Data doesn't lie and shows a factual, not imaginary picture of a driver's driving style and behavior on the road.

While in the traditional insurance model pricing is static and data is collected offline and not aligned with the driver's actual preferences, new technologies such as the cloud, the IoT, and AI allow for these limitations to be effectively lifted.

With them, an offering is created that competes in the marketplace, generates new revenue streams within the company, and builds customer loyalty.

Data-driven innovation - easier said than done. Or maybe not?

The transformation of a vehicle from a traditionally understood mechanical device into a "smartphone on four wheels," as Akio Toyoda once said about modern vehicles, takes time and will not happen overnight. But year by year it already happens, and as the new car models distributed by the big corporations show, this process is actually underway.

Read our article on the latest trends in the automotive industry

The so-called software-defined vehicle that we are developing with our clients at Grape Up is a vehicle that moves through an ecosystem of numerous variables, accessed by different players and technologies.

Clearly, one such provider can be - and should be - the insurer whose products have been tied to the automotive market invariably since 1897, when a certain Gilbert J. Loomis, a resident of Dayton, Ohio, first purchased an automotive liability insurance policy.

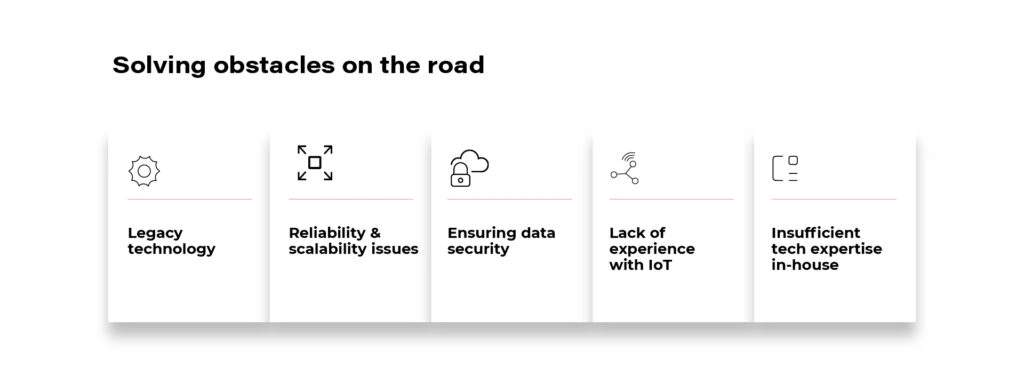

However, for insurance companies to play an integral role in the use of vehicle-generated data, the driver must receive a precisely functioning and secure service from which they will derive real benefits. Without building specific technical competencies and software-defined vehicle knowledge , the insurer cannot achieve these goals.

Only by creating this type of business unit from scratch in-house, or by partnering with software companies, will they be able to compete with insurtech startups like, e.g. Lemonade, which builds their businesses from the ground up based on AI and data analytics .

The right technology partner will take care of:

- data security;

- selection of cloud and IoT technologies;

- and will ensure the reliability and scalability of the proposed solutions.

During this time, the insurer can focus on what they do best - developing insurance competencies and tweaking their offers.

How to choose the right technology partner?

Just as customers are looking for insurance that accommodates their driving and lifestyle, an insurance company should select a technology partner that has more than just technical skills to offer. After all, changing the model in which a traditional insurance company operates does not boil down to creating a digital sales channel on the Internet and launching a modern website. We are talking about a completely different scale of operations requiring the insurance company to be embedded in a completely new, rapidly developing environment.

Therefore they need a partner who naturally navigates the software-defined vehicle ecosystem, understands its specifics, and has experience in working with the automotive industry. Besides, it should be someone knowledgeable about the specifics of the P&C insurance market and the challenges faced by the insurance client.

It is only at the intersection of these three areas: technology, automotive, and insurance, that competencies are built to effectively compete against modern insurtechs.

Like in the Japanese philosophy of ikigai, which explains how to find one's sense of purpose and give meaning to one's work, both companies can build valuable, useful solutions for users. They will bring satisfaction not only to customers but also to the insurance company, which will open a new revenue channel and meet the needs of the market.

Transition towards data-driven organization in the insurance industry: Comparison of data streaming platforms

Insurance has always been an industry that relied heavily on data. But these days, it is even more so than in the past. The constant increase of data sources like wearables, cars, home sensors, and the amount of data they generate presents a new challenge. The struggle is in connecting to all that data, processing and understanding it to make data-driven decisions .

And the scale is tremendous. Last year the total amount of data created and consumed in the world was 59 zettabytes, which is the equivalent of 59 trillion gigabytes. The predictions are that by 2025 the amount will reach 175 zettabytes.

On the other hand, we’ve got customers who want to consume insurance products similarly to how they consume services from e-tailers like Amazon.

The key to meeting the customer expectations lies in the ability to process the data in near real-time and streamline operations to ensure that customers get the products they need when they want them. And this is where the data streaming platforms come to help.

Traditional data landscape

In the traditional landscape businesses often struggled with siloed data or data that was in various incompatible formats. Some of the commonly used solutions that should be mentioned here are:

- Big Data systems like Cassandra that let users store a very large amount of data.

- Document databases such as Elasticsearch that provide a rich interactive query model.

- And relational databases like Oracle and PostgreSQL

That means there were databases with good query mechanisms, Big Data systems capable of handling huge volumes of data, and messaging systems for near-real-time message processing.

But there was no single solution that could handle it all, so the need for a new type of solution became apparent. One that would be capable of processing massive volumes of data in real-time , processing the data from a specific time window while being able to scale out and handle ordered messages.

Data streaming platforms- pros & cons and when should they be used

Data streaming is a continuous stream of data that can be processed, stored, analyzed, and acted upon as it's generated in real-time. Data streams are generated by all types of sources, in various formats and volumes.

But what benefits does deploying data streaming platforms bring exactly?

- First of all, they can process the data in real-time.

- Data in the stream is an ordered, replayable, and fault-tolerant sequence of immutable records.

- In comparison to regular databases, scaling does not require complex synchronization of data access.

- Because the producers and consumers are loosely coupled with each other and act independently, it’s easy to add new consumers or scale down.

- Resiliency because of the replayability of stream and the decoupling of consumers and producers.

But there are also some downsides:

- Tools like Kafka (specifically event streaming platforms) lack features like message prioritization which means data can’t be processed in a different order based on its importance.

- Error handling is not easy and it’s necessary to prepare a strategy for it. Examples of those strategies are fail fast, ignore the message, or send to dead letter queue.

- Retry logic doesn’t come out of the box.

- Schema policy is necessary. Despite being loosely coupled, producers and consumers are still coupled by schema contract. Without this policy in place, it’s really difficult to maintain the working system and handle updates. Data streaming platforms compared to traditional databases require additional tools to query the data in the stream, and it won't be so efficient as querying a database.

Having covered the advantages and disadvantages of streaming technology, it’s important to consider when implementing a streaming platform is a valid decision and when other solutions might be a better choice.

In what cases data streaming platforms can be used:

- Whenever there is a need to process data in real-time, i.e., feeding data to Machine Learning and AI systems.

- When it’s necessary to perform log analysis, check sensor and data metrics.

- For fraud detection and telemetry.

- To do low latency messaging or event sourcing.

When data streaming platforms are not the ideal solution:

- The volume of events or messages is low, i.e., several thousand a day.

- When there is a need for random access to query the data for specific records.

- When it’s mostly historical data that is used for reporting and visualization.

- For using large payloads like big pictures, videos, or documents, or in general binary large objects.

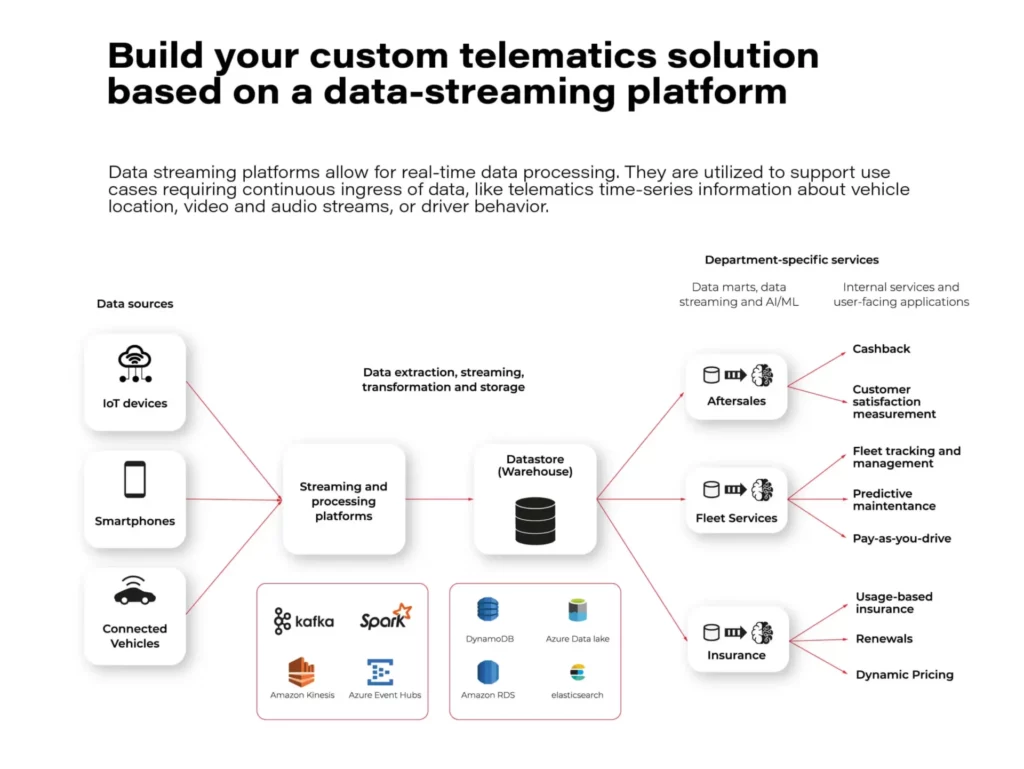

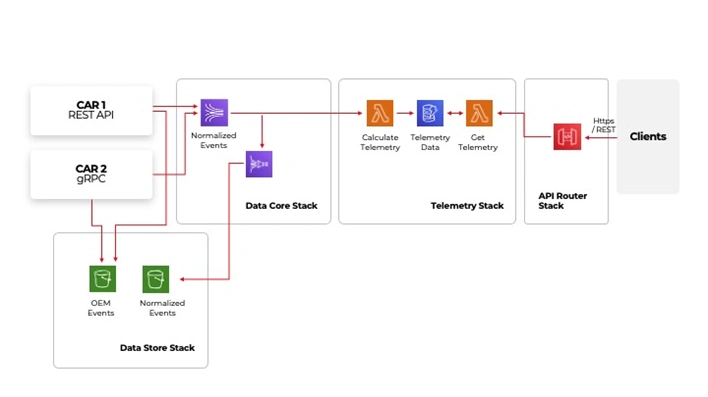

Example architecture deployed on AWS

On the left-hand side, there are integrations points with vehicles. The way how they are integrated may vary depending on OEM or make and model. However, despite the protocol they use in the end, they will deliver data to our platform. The stream can receive the data in various formats, in this case, depending on the car manufacturer. The data is processed and then sent to the normalized events. From where it can be sent using a firehose to AWS S3 storage for future needs, i.e., historical data analysis or feeding Machine Learning models . After normalization, it is also sent to the telemetry stack, where the vehicle location and information about acceleration, braking, and cornering speed is extracted and then made available to clients through an API.

Tool comparison

There are many tools available that support data streaming. This comparison is divided into three categories- ease of use, stream processing, and ordering & schema registry and will focus on Apache Kafka as the most popular tool currently in use and RocketMQ and Apache Pulsar as more niche but capable alternatives.

It is important to note that these tools are open-source, so having a qualified and experienced team is necessary to perform implementation and maintenance.

Ease of use

- It is worth noticing that commonly used tools have the biggest communities of experts. That leads to constant development, and it becomes easier for businesses to find talent with the right skills and experience. Kafka has the largest community as Rocket and Pulsar are less popular.

- The tools are comprised of several services. One of them is usually a management tool that can significantly improve user experience. It is built in for Pulsar and Rocket but unfortunately, Kafka is missing it.

- Kafka has built-in connectors that help integrate data sources in an easy and quick way.

- Pulsar also has an integration mechanism that can connect to different data sources, but Rocket has none.

- The number of client libraries has to do with the popularity of the tool. And the more libraries there are, the easier the tool is to use. Kafka is widely used, and so it has many client libraries. Rocket and Pulsar are less popular, so the number of libraries available is much smaller.

- It’s possible to use these tools as a managed service. In that scenario, Kafka has the best support as it is offered by all major public cloud providers- AWS, GCP, and Azure. Rocket is offered by Alibaba Cloud, Pulsar by several niche companies.

- Requirement for extra services for the tools to work. Kafka requires ZooKeeper, Rocket doesn’t require any additional services and Pulsar requires both Zookeeper and BooKKeeper to manage additionally.

Stream processing

Kafka is a leader in this category as it has Kafka Streams. It is a built-in library that simplifies client applications implementation and gives developers a lot of flexibility. Rocket, on the other hand, has no built-in libraries, which means there is nothing to simplify the implementation and it does require a lot of custom work. Pulsar has Pulsar Functions which is a built-in function and can be helpful, but it’s basic and limited.

Ordering & schema registry

Message ordering is a crucial feature. Especially when there is a need to use services that are processing information based on transactions. Kafka offers just a single way of message ordering, and it’s through the use of keys. The keys are in messages that are assigned to a specific partition, and within the partition, the order is maintained.

Pulsar works similarly, either within partition with the use of keys or per producer in SinglePartition mode when the key is not provided.

RocketMQ works in a different way, as it ensures that the messages are always ordered. So if a use case requires that 100% of the messages are ordered then this is the tool that should be considered.

Schema registry is mainly used to validate and version the messages.

That’s an important aspect, as with asynchronous messaging, the common problem is that the message content is different from what the client app is expecting, and this can cause the apps to break.

Kafka has multiple implementations of schema registry thanks to its popularity and being hosted by major cloud providers. Rocket is building its schema registry, but it is not known when it will be ready. Pulsar does have its own schema registry, and it works like the one in Kafka.

Things to be aware of when implementing data streaming platform

- Duplicates. Duplicates can’t be avoided, they will happen at some point due to problems with things like network availability. That’s why exactly-once delivery is a useful feature that ensures messages are delivered only once.

- However, there are some issues with that. Firstly, a few of the out-of-the-box tools support exactly-once delivery and it needs to be set up before starting streaming. Secondly, exactly-once delivery can significantly slow down the stream. And lastly, end-user apps should recognize the messages they receive so that they don’t process duplicates.

- “Black Fridays”. These are scenarios with a sudden increase in the volume of data to process. And to handle these spikes in data volume, it is necessary to plan the infrastructure capacity beforehand. Some of the tools that have auto-scaling natively will handle those out of the box, like Kinesis from AWS. But others that are custom built will crash without proper tuning.

- Popular deployment strategies are also a thing to consider. Unfortunately, deploying data streaming platforms is not a straightforward operation, the popular deployment strategies like blue/green or canary deployment won’t work.

- Messages should always be treated as a structured entity. As the stream will accept everything, that we put in it, it is necessary to determine right from the start what kind of data will be processed. Otherwise, the end user applications will eventually crash if they receive messages in an unexpected format.

Best practices while deploying data streaming platforms

- Schema management. This links directly with the previous point about treating the messages as a structured entity. Schema promotes common data model and ensures backward/forward compatibility.

- Data retention. This is about setting limits on how long the data is stored in the data stream. Storing the data too long and constantly adding new data to the stream will eventually cause that you run out of resources.

- Capacity planning and autoscaling are directly connected to the “Black Fridays” scenario. During the setup, it is necessary to pay close attention to the capacity planning to make sure the environment will cope with sudden spikes in data volume. However, it’s also a good practice to plan for failure scenarios where autoscaling kicks in due to some other issue in the system and spins out of control.

- If the customer data geo-location is important to the specific use case from the regulatory perspective, then it is important to set up separate streams for different locations and make sure they are handled by local data centers.

- When it comes to disaster recovery, it is always wise to be prepared for unexpected downtime, and it’s easier to manage if there is the right toolset set up.

It used to be that people were responsible for the production of most data, but in the digital era, the exponential growth of IoT has caused the scales to shift, and now machine and sensor data is the majority. That data can help businesses build innovative products, services and make informed decisions.

To unlock the value in data, companies need to have a complex strategy in place. One of the key elements in that strategy is the ability to process data in real-time so choosing the tool for the streaming platform is extremely important.

The ability to process data as it arrives is becoming essential in the insurance industry. Streaming platforms help companies handle large data volumes efficiently, improving operations and customer service. Choosing the right tools and approach can make a big difference in performance and reliability.

How more connected vehicles on the road will impact the insurance industry

By 2023, there will be over 350 million connected cars on the road . What can the insurance industry do about it? It turns out that quite a bit, as automotive companies, introducing the latest technological advances, are enabling new ways to mix driver behavior. This is of great importance in the context of creating offers, but not only. At stake is to maintain the position and competitiveness in the field of motor insurance.

The automotive and car insurance industries are changing

The automotive market is already experiencing changes driven by innovative technologies. More often than not, these are based on the software-defined vehicle (SDV) trend.

If the vehicle is equipped with embedded connectivity, it is able to provide very detailed vehicle and driver behavior data, such as:

● sudden acceleration or braking,

● taking sharp turns,

● peak activity times (nighttime drivers are more vulnerable),

● average speed and acceleration,

● performing dangerous maneuvers.

BBI & UBI and ADAS

Behavior-based (pay-how-you-drive) and usage-based insurance – UBI – (pay-as-you-drive) are the future of car insurance programs . Meanwhile, as vehicles become smarter, more connected, and automated, insurers evaluate not only the driver's behavior but also the car s/he is driving. This evaluation takes into account, among other things, the amount of advanced driver assistance systems (ADAS) that affect the safety of the vehicle's occupants.

Autonomous vehicles

And Deloitte analysts note that self-driving (AV) cars, which are an interesting novelty now but will in time be a standard on par with human-driven vehicles, are also likely to force fundamental changes in insurers' product ranges, as in the risk assessment, pricing, and business models.

Connected cars

Change is already happening, and it will become even more pronounced in the years ahead. IoT Analytics predicts that by 2025, the total number of IoT devices worldwide will exceed 27 billion. Plus, experts predict that there will be 7.2 billion active smartphones and more than 400 million connected vehicles on the road during the same period.

This all clearly shows that we are in an entirely different reality than we were just a few or a dozen years ago. Car insurers need to understand this if they want to maintain their foothold.

Telematics technologies are an obvious step into the future of the insurance industry

Insurance companies have been offering usage-based and behavior-based products for years based on data from either additional devices or mobile apps. This is a fast-growing product area since the UBI market is predicted to be worth more than $105 billion in 2027 , up 23.61% annually.

The best position in this arena is attained by businesses that started investing in telematics technology early and now can take pride in well-developed telematics products.

We are talking about brands such as State Farm®, Nationwide, Allstate, and Progressive. Yet at the same time, companies that deemed telematics a passing trend and therefore didn't invest in it lost a very large amount of market share. The result? Now they have to catch up and race to keep up with the competition.

TSPs understand the potential of connected vehicle data

Insuring companies are not the only ones who recognize the importance of implementing their telematics-based solutions. Telematics services providers understand that value as well, so they invest in building out new capabilities of their products.

This is the case with GEICO , the second-largest auto insurer in the U.S. (right after Progressive). As Ajit Jain, vice president of Insurance Operations at Berkshire Hathaway claims : GEICO had clearly missed the business and were late in terms of appreciating the value of telematics. They have woken up to the fact that telematics plays a big role in matching rate to risk. They have a number of initiatives, and, hopefully, they will see the light of day before, not too long, and that'll allow them to catch up with their competitors, in terms of the issue of matching rate to risk .

Telematics companies see potential in partnering with the insurance industry

Insurance companies are not the only ones who recognize the importance of implementing new data-driven technology solutions. The relationship is two-way, as telematics industry representatives, in turn, are willing to invest in collaboration with insurers and put the customer from this market sector first.

For example, Cambridge Mobile Telematics (CMT), the world's largest telematics provider, has recently announced the expansion of its proprietary DriveWell® telematics platform to networked vehicles. Their flagship software has previously collected sensor data from millions of IoT devices, including smartphones, tags, in-car cameras, third-party devices, etc. From now on, that scope continues to expand by specifically including connected vehicles to create a unified view of driver and vehicle behavioral risk.

This synergy of all acquired data is mainly dedicated to customers in the auto insurance industry, who gain insight into what is happening on the road and behind the wheel. As Hari Balakrishnan, CTO and founder of CMT explains : There is a wave of innovative IoT data sources coming that will be critical to understanding driving risk and lowering crash rates. CMT fuses these disparate data sources to produce a unified view of driving .

Current UBI solutions can be flawed

Existing methods of data collection for insurers also rely on modern technologies, but these can be unreliable. All three methods have their drawbacks: devices plugged into the On-Board Diagnostic (OBD) system, smartphone apps and tags stuck to the windshield.

The first method provides insight into the driver's precise behavior data, downloaded directly from the engine control module (ECM). Weaknesses? The fact that OBD-II devices are limited to the data found in the ECM, for example, while those from other vehicle components remain inaccessible.

In this respect, mobile apps are certainly better, providing insurers with a simple way to launch their own telematics-based program . . In addition, data is collected every time the user drives the vehicle. The disadvantage, however, is that the software does not connect directly to the vehicle's systems. Therefore, the data points are subject to a margin of error, and it also happens that the automatic driving recognition fails and includes in the scoring journeys as a passenger in another car, for example.

Bluetooth-based tags, which is the last solution described here, are installed on the vehicle's windshield or rear window. Like mobile apps, the tags have no direct connection to the vehicle's systems and are therefore prone to bugs.

The conclusions are obvious

Thus, there is a lot to suggest that if an insurer is looking for truly reliable technology, it should opt to use embedded telematics, or data. This is what enables dynamic and, above all, unconditional data collection to reliably assess the risk associated with individual clients.

The data sent by connected cars is more accurate, more detailed, and in much larger quantities compared to other solutions. And this allows insurance companies to better understand customers and their behavior and, based on this information, offer products that are better suited to their needs, as well as more profitable.

Industry insiders don't need much convincing about the advantages of telematics and connected cars over other driver data collection solutions. Data from cars connected to the network are instantly obtainable. Of course, you can enrich it and give it context by using information from smartphones, but in most cases, it is not even necessary. So why invest in something unreliable, which by definition has vulnerabilities and does not meet 100 percent of your needs, when you can opt for a more comprehensive technology that offers more features right from the start.

Considerable importance of connected car data for the insurance industry

Connected car data is the subsequent step in building the ultimate telematics-based products. It is acquired without the need to install additional components. All it takes is a vehicle user's consent to use the data, and then the insurance company obtains the data directly from the OEM.

The information obtained from UBI vehicles can be used successfully and all stakeholders benefit: insurers, as they gain a better understanding of their customers and can better assess risk; OEMs, as it allows them to monetize the data; and finally consumers, who receive a better, more personalized offer this way. J.D. Power points out that 83% of policyholders who had positive claims experience renewed their policies, compared to only 10% who gave negative reviews .

In addition, such reliable data serves not only to improve the profitability of an insurance portfolio, but also to improve road safety. Insurers can offer incentives that will encourage their customers to continuously improve their driving style and increase their care for themselves and other road users.

Even now, market leaders who understand the value of investing in innovation are offering their customers the opportunity to share data from connected cars for UBI/BBI purposes. One example is the State Farm® brand, which offers discounts based on driving behavior. The driver's on-the-road behavior ( sharp braking or no braking, rapid acceleration, swift turns) and driving mileage are automatically sent to the data manager after each trip, so be sure to enable data sharing and location services on your saved vehicle. This information is used to update your Drive Safe & Save discount each time you renew your policy. The safer you drive, the more you can save .

Likewise, Ford Motor Company is increasingly shifting toward using driver data in UBI programs based on connected vehicles. To that end, the automotive giant has partnered with a mobility and analytics brand. Their joint project is expected to empower drivers with more control over how much they pay for their car insurance. Drivers can voluntarily share their driving data from activated Ford vehicles with Arity's centralized telematics platform, and it will then be delivered via Arity's API. Drivesight® to insurers. The obtained risk index can be used to price auto insurance by any participating insurer .

Currently, connected cars are only one option, as many insurance companies are still using, for example, mobile applications in parallel. However, we can already see that the trend of using CC data is present on the market and the number of companies offering such an option to their clients will grow. This is something to be reckoned with.

Significant benefits

For insurers, the benefits are tangible. According to Swiss Re, with 20,000 claims handled per year, the average savings after implementing the above technologies amounted to 10-30 USD per claim .

Telematics also helps to curb so-called claims inflation. Increasingly advanced vehicles are equipped with complex components, which can be costly to replace. Fortunately, today's insurer has the ability to create its own strategy based on the changing cost of spare parts and damage history for major car models. This enables them to develop new pricing that includes inflated compensation costs.

The sooner, the better

Leveraging data and analytics based on artificial intelligence is guaranteed to drive growth. Expanded sources of information improve the customer experience and help streamline operational processes. The benefits are thus evident across the entire value chain. We can confidently say that never before in history has technology been so intertwined with the insurance industry.

That's why all insurance companies should start working on incorporating connected car data into their programs now. The sooner they do, the better positioned they will be when such vehicles become mainstream on the road. After all, the share of new vehicles with built-in connectivity will reach 96% in 2030 .

That's what Evangelos Avramakis, Head Digital Ecosystems R&D, Swiss Re Institute Research & Engagement advises insurance companies to do: Starting small then scaling fast might be a good strategy (...) There is so much you can do with data. But you need to take a different approach, depending on whether you want to improve claims processing or create new products. Conversely, this is what Nelson Tham, eAdmin Expert Asia, P&C Business Management, thinks about implementations: Whenever an SME thinks about digitalization, it intimidates them. But it need not be the case if we start small. They can begin by reviewing their internal processes, see how data flows, turn that into structured data, then analyze this data for more meaningful insights .

How the insurance industry should approach the subject?

Insurers should start by answering key questions like: where connected car data will deliver the most value for my business? What internal capabilities do we have and need? Do we have the required infrastructure, process and skills to leverage connected car data? What investments in technology are necessary to deliver on our goals?

Lastly, they need to consider whether they can better and faster achieve those goals by building required capabilities in-house or working with partners.

A good business and technology partner for the insurance industry is fundamental

Using connected car data is not that straightforward. It requires know-how and the right technology background, as well as finding the right partner to collaborate with.

A well-matched partner will help change the current operating model, by combining automotive and technology competencies and at the same time understanding the specifics of the insurance industry. Some processes simply have to be carried out in a comprehensive and holistic way.

At GrapeUp, we help implement new approaches to an existing strategy. Operating at the intersection of automotive and insurance, we specialize in the technologies of tomorrow. Contact us if you want to boost your business performance.

Interested in our services?

Reach out for tailored solutions and expert guidance.