Personalized Finance as a Key Driver Leading Financial Services Industry into the Future

Personalization in finance is a process that has been steadily developing for the last decade. It’s the most crucial trend you can pay attention to as it captures the essence of what modern consumers want. Individual service and attention.

Personalized finance is a journey with the customer in focus. Getting closer to customers means meeting them where they are, understanding their individual goals, and providing advice they actually want need.

Technology has introduced a tremendous change in personal finance. While it hasn’t yet democratized traditional banking and finance the way it’s promised, it’s well on its way – transforming the way we budget, invest, save or borrow money today. As companies enter the post-pandemic world, they face a consumer landscape undergoing sudden and radical change. Customer expectations have been transformed to make “anywhere, anytime” the norm. Achieving personalization at scale will be definitely one of the biggest challenges for traditional institutions in the race to differentiate through a digital channel in the coming years.

Why personalization matters in Financial Services?

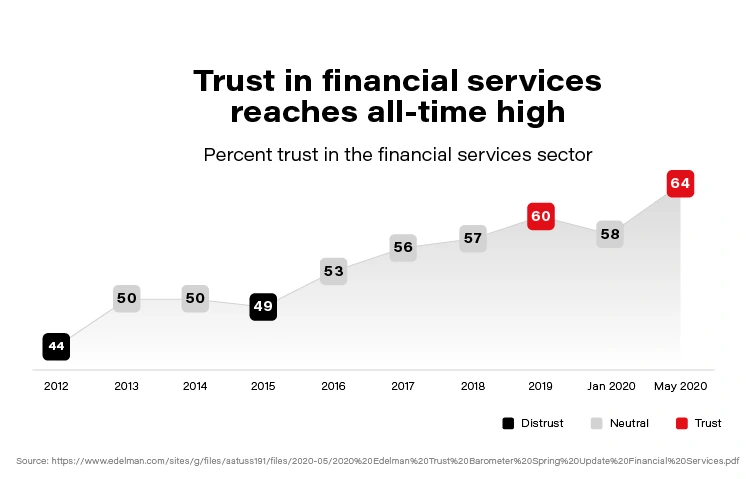

Personalized services shorten significantly the distance between a financial organization and its users, and are based on trust. The more we trust the product the more we are eager to share our personal data in order to receive a tailored, highly individualized service that maximizes value for customers. Trust is still the strongest word in banking. The 2020 Edelman Trust Barometer Spring Update: Special Report on Financial Services and the Covid-19 Pandemic reveals that the public’s trust in financial services has reached an all-time high of 65 percent amid the pandemic.

Now, when we associate the trust clients put i.e., into banks with the scale of daily operations (counted in millions), we easily conclude that there is an enormous opportunity in front of the financial sector to build highly personalized products and enable customers to realize their financial wellbeing potential.

With an increasing demand for more personalized experiences and focus on sustainability, Banks, Insurers, or Asset Management organizations are reaching the limits of where their current technology can take them with their business transformation initiatives. Therefore, it’s more critical than ever for Financial Institutions to turn towards Data and AI and get the most out of it – to meet these demands.

While reading different collaterals for the purpose of this article, we noticed an interesting paradox related to the financial domain. According to the variety of global innovation studies (i.e., Forbes Most Innovative Companies or The Global Innovation 1000 study), the Financial Services domain lacks innovation for nearly two decades. On the contrary, it has consistently been the most profitable sector in FORTUNE GLOBAL 500!

Data and AI for personalized finance

To make sure an organization stands out of the competition in an ever-changing financial environment and understands its customers better, it should radically change its approach to Data & AI utilization. Although traditional banks and financial enterprises differ by size, market dynamic, or type of services offering – there is a common set of requirements (attached below) worth taking into consideration when pivoting towards better personalization which can be achieved thanks to the advanced use of Data & AI within an enterprise:

- The Executive Board must believe that Data & AI will make a difference, and this commitment requires long-term investment/research.

- Organizations need to find a Champion that can lead a data/AI team, but at the same time be able to talk to the business stakeholders and articulate the benefits of the models *tools* being implemented.

- It’s necessary to spend time to create Data Strategy, determine a toolset, and figure out when to use Data vs. Analytics vs. AI. Without a strategy, an organization is flying blind and wastes precious time/resources *money*.

- Focus on what brings real value to the organization. Build a use case backlog that balances return on investment, time to market, innovation, and data availability. All of these are important and can help an organization determine where to start and why.

- Data Ethics, Privacy, and Governance are critical to not just the organization but its customers. Use their data inappropriately or violate their privacy even once, and you risk forever damaging the relationship (see recent case of Robinhood).

- Don’t assume you can do it by yourself. Consider hiring, engage with a consulting partner, outsource – all of the above are likely required.

How does technology help achieve personalization at a large scale?

Commonwealth Bank of Australia and Royal Bank of Scotland are early adopters in the traditional banking ecosystem when it comes to personalized CX. These companies use advanced data analytics coupled with artificial intelligence to offer personalized experiences – technology that allowed them to determine and deliver ‘the next best conversation’ at scale saw a 30 to 40 percent increase in sales, back in 2017!

Personetics, a data-driven platform that uses AI to help banks issue personalized advice and insights to customers, has raised $75 million in funding from private equity firm Warburg Pincus. Founded out of Israel in 2010, Personetics offers technology that works inside financial institutions’ software. It aims to analyze customers’ financial transactions and behavior and deliver real-time tips and suggestions to improve their longer-term financial health.

In the latest report related to digitalization at Handelsbanken (one of the largest European banks with HQ in Sweden), we see practical examples of how technology played a vital role in building highly personal advisory services, which increased the customer value and realize the potential in their 35 million digital meetings per month by utilizing data and treating each customer as an individual.

Thinking about the scale and impact of the financial business, there was no better time in human history to maintain simultaneously hundreds of millions of interactions to deliver value per individual need. Advancements in automation, cloud computing, or machine intelligence technologies create new space for maximizing the power of data and give an enormous opportunity for traditional businesses to exponentially grow the quality of relationships and keeping up with customers.

It’s very hard to compete with an organization that is capable to save its clients precious time and deliver value which is a sum of trust + context + momentum in an engaging and simple to consume form.

Head of Digital at Bank of America, David Tyrie, shared an interesting viewpoint that refers to personalization challenges for the traditional banking ecosystem during discussion at the Digital Banking 2020 Conference:

Tailoring client experiences 1:1 to feel timely, relevant, and credible requires real-time decisioning of transactional, contextual, and behavioral data and an adoption of open platforms so that information can flow to trusted partners. “Closed-loop, data ecosystems” can help realize hyper-personalization at scale because they enable continuous learning to serve customized and contextual experiences, content, offers, recommendations, and insights.

This continuous learning component is vital as it helps big organizations like banks or insurers build more individualized interaction with their customers and learn their behavior along the way. We already see a growing post-pandemic trend to emulate everything that’s physical and build a digital representation of physical relationships to make sure the customer is at the heart of financial transformation.

Obstacles and opportunities for personalized finance

Personalization requires financial organizations to jump multiple levels when it comes to data maturity. In order to win the race for customer attention in 2021, companies should become not only a data organization from the ground up but to be flexible and fast with implementing new structures (incepting necessary cultural shift), systems and competencies (digital skills) that distinguish them from the old legacy times.

Even though increased focus on customers brings obvious benefits for both the organization and its clients, there are several significant challenges before financial enterprises can reap the great benefits from personalization. It’s worth making sure the organization is prepared and can handle some of the existing challenges:

- Data consists of a lot of unstructured content, which makes it difficult to interpret.

- Instead of considering data as an IT asset, the ownership of data should be moved to the business users, making data a key asset for decision making (it’s necessary to strengthen cooperation between business & tech, to tear down the product-silos).

- Restrictions of regulatory requirements and privacy concerns.

- Integrating customer data from multiple sources to create comprehensive profiles that are then used by predictive analytics tools to generate the most relevant recommendations and products might cause data quality issue due to third-party, publicly available data sources for which financial services companies can’t manage the reliability.

It seems unreal that the successful banks and financial industry organizations of tomorrow will be that far removed from those of today. Rather how customers interact with them will be different (digital customer interface). Financial services have become anything but personal. The relationship we have with our money is being completely reimagined for the digital world, same as how we go about building financial services is changing. We are sure this trend will not only grow but will be one of the key drivers in the financial services transformation.

Is it insightful?

Share the article!

Check related articles

Read our blog and stay informed about the industry's latest trends and solutions.

see all articles

Leveraging AI To Improve VIN Recognition – How To Accelerate and Automate Operations in the Insurance Industry

Read the article